With heads likely still a little sore after welcoming in the new year, the International Energy Forum (IEF) offered some sobering words. “Our electrical infrastructure is built on copper,” it said, “placing this metal at the core of the energy transition.”

It is a statement you would be hard pushed to counter given that for the past two centuries or so, copper has been the backbone of electrification and innovation – beginning with its now seemingly rudimental ability to conduct electricity in wiring.

Today copper plays a far more inventive role. It is used in an infinitude of ways, from cabling and components to motors and batteries – the latter proving to be the hottest of property right now. Indeed, the International Energy Forum (IEF) declared that “the future of energy will be built on copper”, citing the likes of electric vehicle (EV) charging infrastructure and grid-scale energy storage, as the world powers towards wide-scale energy transition.

So, is copper – more specifically the copper-producing industry – up to the task? The IEF is not so sure, warning a sluggish supply could “compromise ambitions to decarbonise the energy sector” and that producers need to “take unprecedented action” if the challenge is to be met.

Part of that extraordinary response would include, it argues, making history by opening three ‘tier-one’ mines every year until the mid-2050s, costing half a trillion dollars in the process. Either way, the international organisation with 72 energy minister members from producing and consuming energy nations says there is no simple solution to what it calls a “looming global shortage”.

These are, on the face of them, fair concerns. The International Energy Agency (IEA) says clean energy technologies, including low-carbon power generation, electricity networks, EVs and storage and hydrogen, accounted for a quarter (24%) of copper demand last year.

It believes that will grow to almost half (45%) by 2030 and to more than 50% by the end of the next decade if its pathway to net-zero carbon emissions in the energy sector, or Net Zero Scenario, is met. “Under the Scenario this would equate to a compound annual growth rate (CAGR) in copper demand for clean energy technologies of 6.9% from 2023 to 2040, versus flat demand from other uses,” explains David Kurtz, director of mining and construction at GlobalData, a market analysis and intelligence provider.

Copper moves from deficit to surplus, despite Panama mine closure

Kurtz appears more optimistic than the IEF about the ability of the mining sector to rise to the challenge.

“While copper has been in deficit in recent years,” he says with a nod to the challenges the industry has faced, “the International Copper Study Group’s projections as of April 2024 are for a world refined copper balance surplus of about 162,000 tonnes (t) for 2024, and 94,000t for 2025.”

GlobalData is forecasting total mined copper production to reach 23.4 million tonnes (mt) in 2024, a 3.5% increase on last year.

For its part, GlobalData is forecasting total mined copper production to reach 23.4mt in 2024, a 3.5% increase on last year.

Now accounting for more than 10% of global production – thanks to the ramp up of new mines such as Kamoa-Kakula and Kisanfu – the Democratic Republic of Congo (DRC) is expected to help drive that growth. Other regions helping to add volume include Chile and the US, where capacity fell a little in 2023.

There is, though, a slightly more cautionary tone from Kurtz: “Year-on-year growth will be limited, however, by the closure of the Cobre Panama mine in late 2023.”

First Quantum’s $10bn (C$13.8bn) copper mine in the Panamanian jungle had been dogged with issues almost since it was mooted. They included legal and taxation concerns, compounded further still by political instability and recession in recent years.

The mine finally stopped operating late last year after widespread protests and what has proved to be an almost fatal breakdown in relations between the mine’s owners, the country’s political elite, its judicial system and even its citizens.

It came at a time when the mine’s production had accelerated massively, with 2023 by far smashing records in terms of its annual output since it opened in 2019. It is a story with an impact that continues to be felt across the copper-producing industry.

The growing need for new copper production capacity

The closure of the mine comes at a time when, as Kurtz puts it, “there is a growing need to bring new copper production capacity online”, but, he says, First Quantum Minerals’ plight is just one factor.

“Under the Net Zero Scenario, the IEA forecasts that demand for copper could reach 39 million tonnes per annum (mtpa) by 2040, with at least 19.6mtpa being driven by clean energy. This means more than 13mtpa of supply will need to be found between 2023 and 2040 to fulfil the requirements of this scenario.”

It is easy to gloss over figures like these, not really understanding the practical significance; but that is twice the increase in copper output achieved in two decades to 2020, a huge challenge given the rising costs of development and declining grades, says Kurtz.

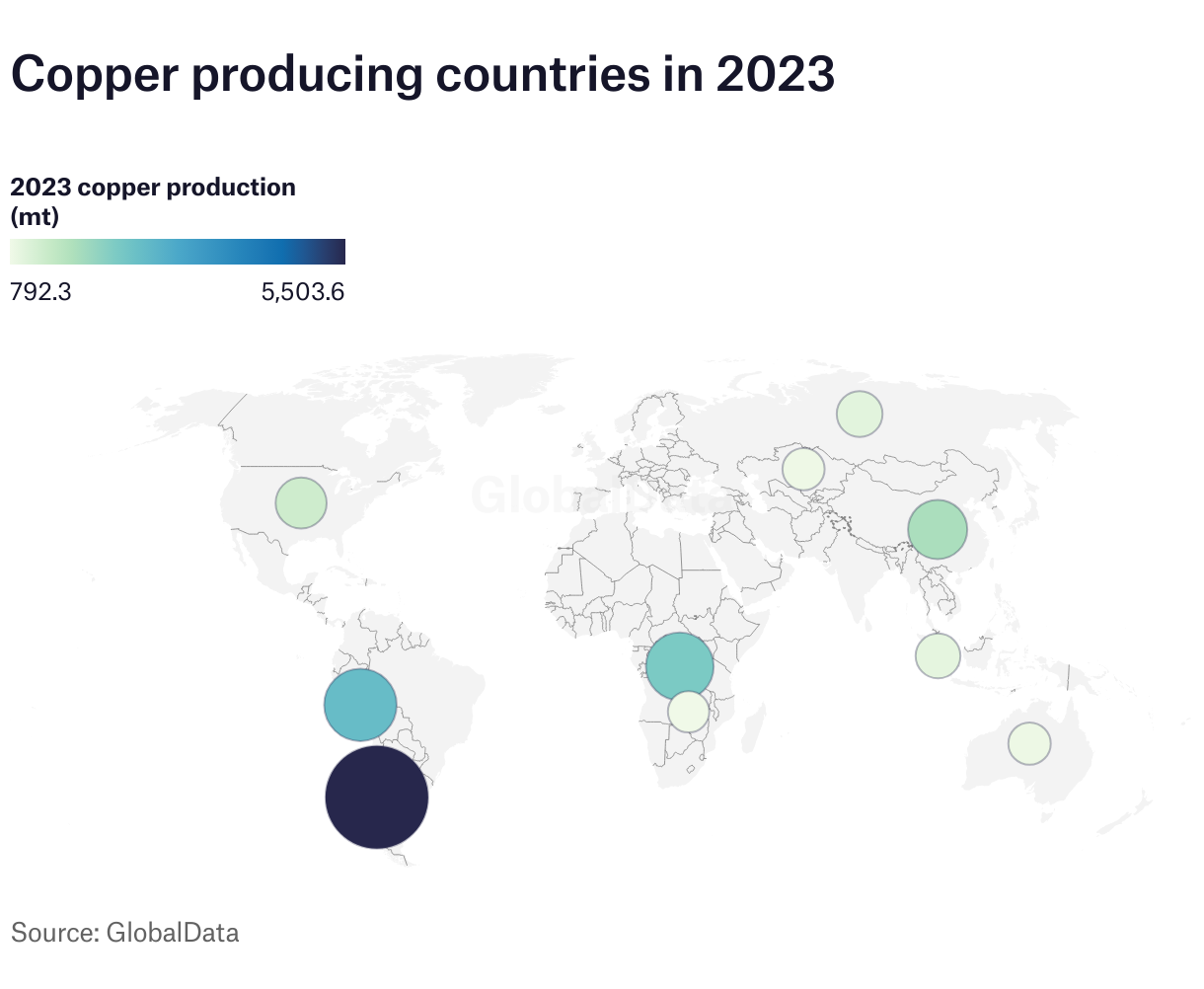

GlobalData figures support that, showing that the growth in global production has remained relatively slow but steady, typically adding around two million tonnes every five years. As of last year, the world’s biggest copper supplier was Chile, notching up more than 5.5mt.

The leading supplier was Freeport-McMoRan – owner of two of the world’s ten largest copper mines, Cerro Verde in Peru (third biggest) and Morenci in Arizona, US (eighth) – which collectively produced almost 2mt. BHP ranked second, supplying 1.78mt of copper to market in 2023. Chile’s Codelco was third, producing 1.42mt.

The Cerro Verde Mine came in third of the 709 currently operating mines globally, according to GlobalData, producing an estimated 444,000t of copper. It was headed by BHP Group’s Escondida Mine in Chile, which produced 882,100t. Glencore’s Collahuasi Mine, also in Chile, came in second with an estimated output of 563,390t of copper in 2023.

Major opportunity for producers

Although the numbers sound colossal, concerns remain that the market will likely be found wanting in years to come. Kurtz and GlobalData, although less pessimistic, flag other potential issues down the line.

“Over the remainder of the decade growth in demand for copper is expected to outstrip demand growth for other metals such as lead, zinc and iron ore,” Kurtz says, “with just nickel and lithium of the major commodities expected to witness higher growth demand.”

For copper miners, rising demand and consequentially high prices represent "a major opportunity”.

However, this should not be seen in a negative light by the copper supply sector. For copper miners, rising demand and consequentially high prices – which hit an all-time high in the second quarter of 2024 – represent what Kurtz says is “a major opportunity”, with many looking to invest even more in existing and developing copper mines and other critical minerals.

“That said, developers have been slow to grow supplies due to a combination of long lead times and high costs to develop new mines, and the industry’s attempts to reduce its own environmental footprint and address ESG [environmental, social and governance] concerns within copper mine host countries,” Kurtz adds.

To this backdrop, GlobalData forecasts production to moderately grow between 2023 and 2030, increasing at a CAGR of 2.7%. Equally, consumption is expected to outpace that at a 3.3% CAGR over the same period.

Kurtz says that although the IEA expects secondary supply and reuse will help alleviate demand by 2030, the International Copper Association still estimates supplies could fall 1.7% short of demand as early as the next decade.

How is geopolitics impacting the copper market?

There is another noteworthy consideration too: geopolitics. International relations are becoming increasingly strained and with political uncertainty over coming months looking set to play a part too, there is every chance disharmony and perhaps even conflict could become a hurdle.

Russia, the world’s sixth-leading copper producer, and China, which has considerable vested interest in the DRC’s copper mining industry and refines almost half the world’s supply, do have the ability to influence the market. “The geographical concentration of copper’s processing particularly makes the metal vulnerable to factors such as geopolitical disruption,” warns Kurtz.

It is clear that copper mining will remain an essential part of a modern world looking for energy transition. It is, though, also clear that at best it can only hope to keep pace with that demand; that said, there are many other less favourable scenarios not to be ignored.