Australia has a national target to reduce emissions by 43% compared with 2005 levels by 2030 and to achieve net zero by 2050. The mining sector, which accounted for almost a quarter of the country’s emissions in 2022, has a large role to play.

Like other signatories to the Paris agreement, Australia is currently developing its 2035 emissions reduction target so it can update its nationally determined contributions by next February’s deadline. This will be supported by six sector-specific decarbonisation plans covering major industry including mining/resources.

Go deeper with GlobalData

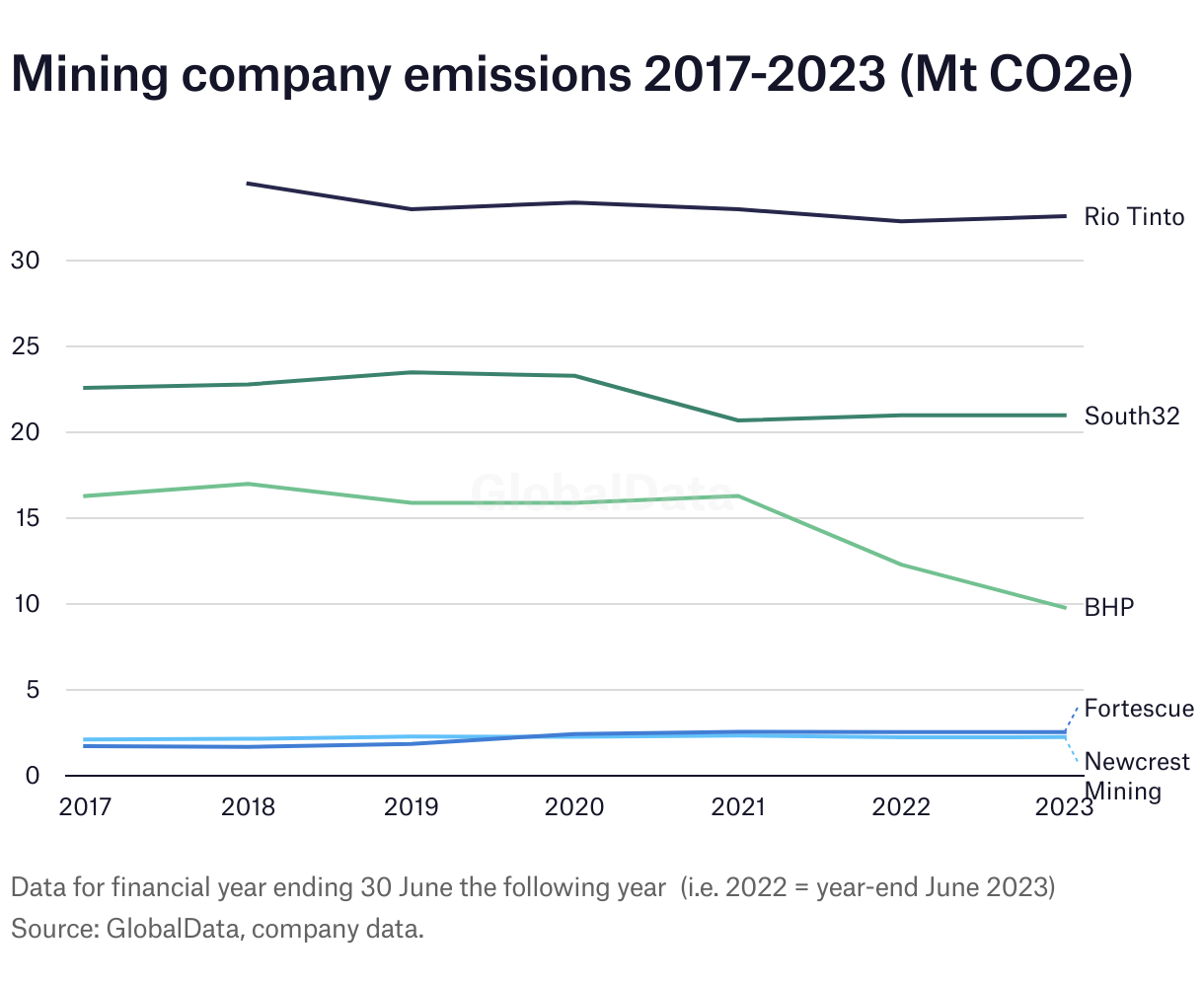

Emissions from Australia’s mining industry

Emissions from Australia’s resources sector, comprising mining and oil and gas (O&G) operations, reached 99 million tonnes (mt) of carbon dioxide equivalent (CO₂e) in 2022. This equated to 23% of the country’s total emissions, according to the Climate Change Authority (CCA), an independent statutory agency responsible for providing advice to government on climate policy.

Fugitive emissions from coal mines (mostly underground) were the biggest contributor, producing 25% of the resource sector’s emissions. Diesel fuel combustion at mines, mostly related to haulage fleet and equipment, accounted for 20% of emissions. On-site power across mining and O&G was responsible for 11%. Decarbonisation of the sector requires “widespread electrification and [the] deployment of fugitive abatement technologies in oil, gas and coal mining”, the CCA states.

Australian mining companies are moving quickly to cut emissions. Today, most miners have set 2050 as the target year for achieving net-zero carbon emissions, according to Martina Raveni, a strategic analyst at GlobalData.

Shorter-term emission reduction goals “typically aim for around a 30% reduction by 2030”, she adds, although some have more aggressive ambitions. Fortescue is targeting net zero for scope 1 and 2 emissions across Australian iron ore operations by 2030, while Rio Tinto is aiming for a 50% reduction in emissions versus the 2018 baseline by 2030.

“Mining is a difficult sector to decarbonise,” Raveni says. “That said, shifting power sources is the main game in town for the mining industry.”

Increasing the share of renewable energy consumption is proving to be a primary way to achieve operational emissions reduction in the short term, as illustrated by BHP and Harmony Gold. Cuts can be facilitated through power purchase agreements (PPAs) or installing on-site renewables such as wind or solar.

Ditching diesel at Australian mines

Diesel displacement will also be important for mining companies to tackle scope 1 and scope 2 emissions. Data from BHP indicates that 61% of the company’s operational GHG emissions came from diesel in the 2024 fiscal year.

“The mining industry’s long-term strategy for displacing diesel is full electrification of the fleet, which will be gradually phased in over ten to 15 years,” says Jordan Strzelecki, strategic analyst at GlobalData.

“This shift has already begun, with small diesel-powered haul trucks being slowly replaced by battery-electric and hydrogen fuel-cell alternatives.”

A “notable step forward” in this transition occurred in September 2024, Strzelecki says, referring to Fortescue’s landmark $2.8bn (A$4.29bn) deal with OEM Liebherr to jointly develop and validate a zero-emission fleet. The deal was announced at MINExpo INTERNATIONAL, which took place in Las Vegas, US, from 24 to 26 September.

The collaboration will deliver 475 electric Liebherr machines to Fortescue’s operations in Western Australia, replacing around two-thirds of the diesel fleet. Liebherr and Fortescue will also implement an autonomous battery-electric haulage solution for large-scale mining operations, to be validated in early 2025.

Fortescue says the technology “will be [made] available to the rest of the mining industry in the near future”. The world’s largest iron ore producer is targeting “real zero” by 2030 at its Australian iron ore operations.

Several mining companies have also proposed the use of sustainable fuels as a transitional decarbonisation strategy. However, barriers remain, with Glencore telling a consultation that biofuels “are currently cost prohibitive, supply constrained and have a range of issues in relation to ethical providence, which may make them unsuited for large scale deployment and use”.

Others have called on government to adopt frameworks that support the wider adoption of biofuels.

The CCA also points to pre and post mine drainage in underground coal mines as an emissions reduction strategy. Various other technologies are also being explored for this purpose.

Emissions reductions progress

Many miners have reduced their emissions over the past five years, according to data from GlobalData, Mining Technology’s parent company. However, challenges remain, and it is not clear whether emissions will continue to fall in the near term.

BHP has already achieved its 2030 target of at least a 30% reduction in operational emissions compared with fiscal year 2020 (FY2020). This drop was mostly driven by the reduction in scope 2 emissions at its copper operations, achieved through renewables PPAs.

However, recent figures from the company’s Climate Transition Plan 2024 predict that scope 1 and 2 emissions could rise by 3% between FY2024 and 2030, considering the range of uncertainty.

Additionally, in line with its plan to achieve ‘real zero’, Fortescue projects that scope 1 and 2 emissions across its Australian iron ore operations “will continue to rise until around FY2026, before they begin to fall in response to the scaling of decarbonisation activities”, mainly driven by an increase in operational expansions such as at Eliwana, plus construction at the Iron Bridge magnetite mine, which produced its first ore in May 2023.

According to the CCA, several barriers remain, ranging from hesitance to pay a “green premium” to the lengthy approval process for renewable energy and related infrastructure, and supply chain uncertainties related to the availability of electric mining equipment and low-emissions fuels.

A shortage of skills needed to support decarbonisation of mining may also prove a challenge, with a predicted increase in demand for electrical and trade skills and the continued shift towards automation requiring “higher order capabilities across analytics and data science”.

With Australia bidding to host COP31 in 2026, all eyes will be on the country’s delegation in Baku, where it has an opportunity to demonstrate its climate leadership on a global stage.

As Matt Kean, chair of the CCA, said in September, the country “needs to seize this once-in-a-generation opportunity to ensure Australia’s rapid and orderly transition as the world transforms to avert the worst impacts of climate change”.

This will require a major reorganisation of supply chains, production systems, industrial zones, energy sources, public and private finance, infrastructure and workforces, in which the mining/commodities sector will have a significant role to play.