The modern battlefield is not only shaped by advanced weaponry and sophisticated technology, but also by the critical minerals that make these innovations possible.

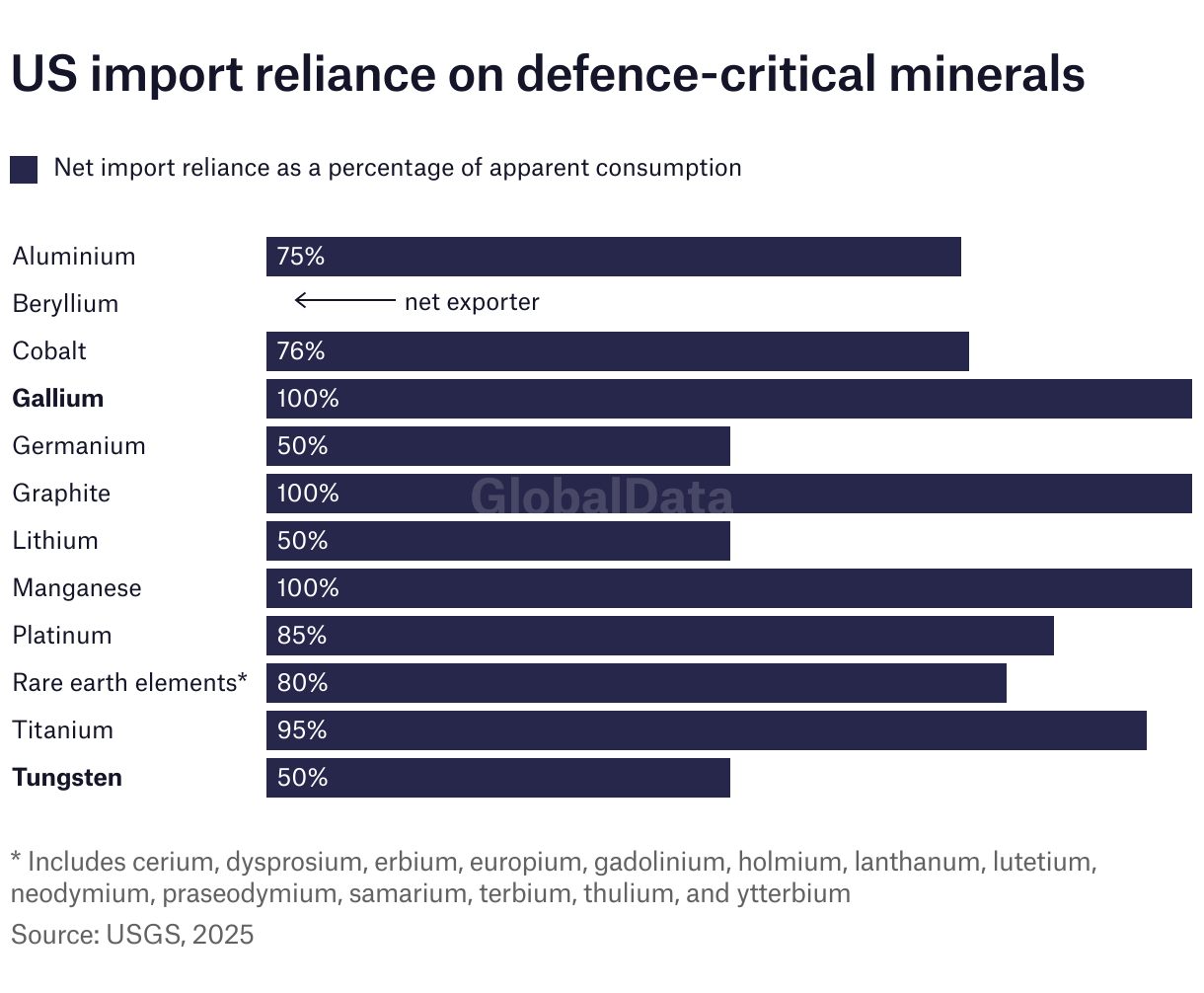

In December 2024, NATO published a list of 12 defence-critical raw materials ─ aluminium, beryllium, cobalt, gallium, germanium, graphite, lithium, manganese, platinum, rare earth elements (REEs), titanium and tungsten ─ that form the backbone of military hardware.

Go deeper with GlobalData

These critical minerals are indispensable for the jet engines of fighter aircraft and the semiconductors in missile guidance systems. There is a problem, however: China controls 60–90% of global processing capacity for many of them.

The race to secure alternative sources has intensified, particularly considering China’s recent export restrictions on gallium and germanium, two elements critical for military-grade electronics.

This growing resource war is being fought against the backdrop of the ongoing Russia-Ukraine conflict, which has further highlighted the West’s vulnerability. Now, a controversial minerals deal between the US and Ukraine aims to break this dependence.

This raises several questions, chief among them being can NATO allies truly regain control over their supply chains, and what will the cost of this new scramble for resources be?

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataTungsten: an indispensable metal of war

Among the critical minerals listed by NATO, tungsten has emerged as one of the most strategically significant.

A September 2024 report from the US Government Accountability Office (GAO) states that tungsten is essential for military applications, particularly in armour-piercing munitions and missile systems.

Lewis Black, CEO of Almonty Industries, a tungsten supplier, starkly put it: “If you want to drop something particularly unpleasant from a drone to eviscerate a car, you need tungsten.

“If you want to manufacture any munitions, whether artillery shells, through all the calibres, right down to small calibre, you need tungsten for the penetrators.”

The GAO report highlights that the US Department of Defense (DOD) has assessed tungsten as a mineral with a high potential for supply chain disruption.

China controls around 85% of the global tungsten supply, leaving Western defence manufacturers alarmingly exposed. Yet, despite its military importance, the US has almost no domestic tungsten production. Over the past three years, the primary imports of the metal to the US have been from China (27%), Germany (14%), Bolivia (8%) and Vietnam (8%).

Black describes the situation as a supply chain vulnerability that has long been ignored: “The problem that the West faces is that there are very few tungsten options available. It was always an unwritten rule in our sector not to really weaponise or politicise tungsten, but it appears that China’s strategy with tungsten is to starve Western consumers.”

The Pentagon has attempted to counter this through stockpiling and investment in alternative sources, but as Black warns: “We can produce the finest, technically advanced military equipment in the world, but without tungsten, we cannot produce anything.”

Gallium: the silent engine of military electronics

Another crucial mineral in the defence sector is gallium, a component in advanced radar systems, missile guidance and electronic warfare.

A 2024 report from the Center for Strategic and International Studies (CSIS) warns that China’s decision to impose export restrictions on gallium has already disrupted Western defence manufacturers.

“There are 3,800 military uses for gallium – and there is only a small stockpile in the US and no domestic production,” explains Harvey Kaye, director of US Critical Materials, which recently reported high concentrations of gallium (180–385 parts per million) at its Sheep Creek project in Montana, US.

With China accounting for more than 98% of global gallium production, the export restrictions imposed in 2024 have left US defence manufacturers scrambling.

While alternative sources exist, including Ukraine and Greenland, western nations seem years behind in building independent gallium supply chains. The consequences of this delay could be profound, with potential disruptions to the production of radar systems, electronic warfare capabilities and next-generation missile defence technologies.

According to GlobalData’s strategic intelligence report on critical minerals, China has spent decades securing control over the supply chains of key materials. The report reveals that between 2019 and 2024, China invested $33.9bn (239.19bn yuan) in mining-related foreign direct investment projects, focusing on securing access to lithium, graphite, nickel and cobalt.

“Banned Chinese items are used in several aspects of the defence industry. From artillery rounds to advanced radar systems, Chinese-dominated critical minerals are strategically paramount to defence firms,” says Aidan Knight, associate analyst, strategic intelligence at GlobalData.

“Ukraine has supplies of antimony, graphite, gallium and germanium to make up for the shortfall caused by Chinese export restrictions, yet China still dominates critical mineral production and processing,” he adds.

The US-Ukraine deal: a geopolitical gamble

The proposed US-Ukraine critical minerals and rare earths deal is one of the most significant and recent developments in this global scramble for defence-critical minerals.

The agreement has been widely discussed in diplomatic circles. US President Donald Trump’s February 2025 X statement made it clear that critical minerals were at the heart of the latest US-Ukraine negotiations.

— Donald J. Trump (@realDonaldTrump) February 24, 2025

Ukraine’s vast mineral reserves, including titanium, REEs, lithium and gallium, could make it a prime candidate for reducing Western reliance on China.

The deal is also seen as a move to ensure that the billions of dollars in military aid sent to Ukraine during the ongoing conflict can be leveraged into long-term economic and security benefits for the US.

However, the agreement has raised concerns about its potential impact on the fragile geopolitical landscape.

“Developing mine sites and sufficient infrastructure in the war-torn nation will take time, potentially decades,” says Knight.

“It is unlikely that a mineral deal with Ukraine will be able to secure a stable supply of critical minerals to meet expanding defence and energy transition needs quickly,” he claims.

The new resource war: can the West fight back?

Recognising these vulnerabilities, NATO and its allies have begun strengthening critical minerals supply chains.

Yesterday (21 March), Trump signed an executive order invoking emergency powers to enhance domestic production of critical minerals under the Defense Production Act. This law from the 1950s, grants the US DOD authority to secure equipment for national defence.

The executive order directs federal agencies to identify mines for quick approval and federal lands suitable for mineral processing. It also expedites permitting for mining and processing projects and instructs the Interior Department to prioritise mineral production on federal land.

The Defense Advanced Research Projects Agency (DARPA) has launched initiatives such as the Open Price Exploration for National Security programme, which leverages AI-powered predictive technology to assess global mineral supply and demand.

Charles River Analytics, a company awarded a $4.5m DARPA contract, is developing probabilistic models to increase transparency in the critical minerals market. One of the most ambitious initiatives is the “mine-to-magnet” strategy spearheaded by the DOD, which aims to develop a fully domestic rare earth supply chain.

Western nations remain highly vulnerable to critical mineral supply disruptions despite growing investments and policy initiatives.

As industry leaders such as Lewis Black caution, more decisive action is needed.

“We are trying to break that addiction [to Chinese supply] because… like all addictions, it is unhealthy. We cannot afford to go cold turkey because we are just not strong enough to do it,” he says.

One thing is certain: the defence industry has never needed the mining sector more than it does today.

As governments and corporations navigate this new era of resource competition, the ultimate question remains: can the West secure its critical minerals before China tightens its grip even further?

The fight for critical minerals is just beginning – and its outcome will shape the future of global military power.